With total investment reaching RMB 100 trillion (EUR 12 trillion) in 2012, China’s construction market is enormous and will keep growing quickly in the foreseeable future. Currently, the country is constructing more than one third of all buildings worldwide, with added square meters of living space amounting to the equivalent of a city like Rome in about two weeks and a country like the UK or Spain every single year. A recent sector report published by the EU SME Centre identifies a number of factors indicating that the sector will continue to be one of the main drivers of China’s growth, providing European SMEs offering high-quality products sustainable opportunities in selected niche markets.

Forecasts for selected indicators in China’s construction sector

|

Indicator |

2013f |

2014f |

2015f |

|

Construction % in GDP |

5.4% |

5.3% |

5.2% |

|

Total output value of construction (RMB bn) |

14,584 |

16,772 |

19,456 |

|

Construction output growth (%) |

13% |

15% |

16% |

|

Output value of building construction (RMB bn) |

838 |

947 |

1,079 |

|

Growth of output value of building construction |

12% |

13% |

14% |

|

Value added of construction (RMB bn) |

2,781 |

2,976 |

3,214 |

|

Growth of value added of construction (%) |

10% |

7% |

8% |

Source: EU SME Centre report The construction sector in China

Controlled environment – the impact of government policy

The overall development of the market will depend strongly on future regulatory interventions by the authorities. On one hand, the nationwide campaign for continued urbanisation will maintain the construction sector’s current significance for China’s overall economy in the coming years. By 2025 the government wants 70% of its citizens to live in cities, which would entail a mass migration of 250 million people in the next 12 years as well as massive efforts to provide housing and adequate infrastructure for all of them. On the other hand, the desire to decrease the country’s dependence on public investment and increase domestic consumption could dampen the sector’s prospects in the long run.

Government policy is also influencing the geographic distribution of construction activities. More than 85% of revenue is still generated in the eastern metropolitan areas, but because of governmental investment incentives, fast growth and large-scale infrastructure projects, western regions and second and third tier cities are quickly catching up. Nevertheless, the largest markets for most European products are still located on the eastern seaboard.

Home field advantage – domestic players own the market

Construction is carried out almost exclusively by large Chinese companies, with private enterprises dominating the construction of buildings (81% market share) and state-owned enterprises heavily involved in infrastructure projects (18% market share). Foreign companies occupy a meagre 1% of the market, a share which has actually been decreasing over the last five years. The EU SME Centre report identifies three main challenges that hinder western companies looking for large-scale involvement in the sector:

1.) Regulation

Foreign and even newly established Chinese companies experience strong regulatory constraints. Licences for construction firms are especially hard to come by and new materials and methods are often prohibited due to the country’s limited ability to assess the benefits of their application.

2.) Common business practices

As in many other sectors in China, being well-connected in business and politics is often more important than product and service quality. Because business is to some extent promoted through practices not acceptable to western companies, advantages like higher quality, innovative products and established business processes are not always sufficient to level the playing field.

3.) Price competition

More often than not, price is the main factor influencing the decision making process of builders in China. As builders and buyers are usually not the same people, quality consciousness and total cost of ownership rarely enter the equation.

Fringe business – foreign companies in the sector

Foreign companies will find opportunities mostly in upscale niche markets, as Chinese consumers tend to associate European products with characteristics like reliability, design and innovation, and are willing to pay premium prices for them. Three trends in particular will increase demand for sophisticated European products in respective markets:

1.) Labour efficiency

Due to increasing costs, builders are forced to pay more attention to labour efficiency. This will push demand for building systems like precast, equipment for building material production and general mechanisation, sophisticated and low maintenance building materials as well as training in corresponding processes and technologies.

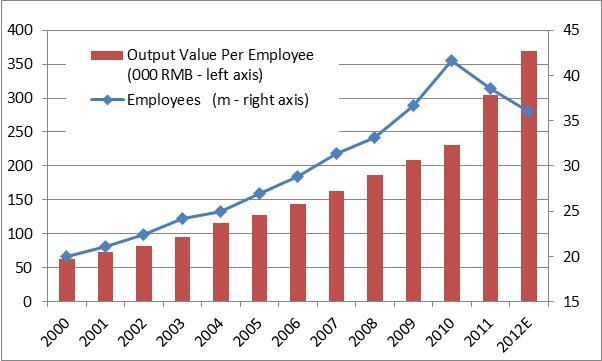

Labour productivity in China 2000 – 2012

Source: EU SME Centre report The construction sector in China

2.) Energy efficiency and green building

Experts estimate that China will become the world’s largest market for green buildings by 2017. The central government has set precise targets for energy saving and eco-friendly buildings. Although not yet a dominant feature in residential construction, many public buildings have to adhere to stringent energy norms and builders are implementing a large range of energy conserving or generating technologies. This, in combination with the introduction of the Chinese Green Building Standard, is causing an annual growth rate of 60% in the green building sector, compared to a general market growth of about 5%. Opportunities for European companies include efficient lighting and heating systems, smart measuring and control systems, energy storing technology and retrofitting services. To find out more about green building in China, see our sector report, which will be available on our website shortly.

3.) Design and quality

Because of rising expendable income levels and an increasing desire to live comfortably, top-quality design products that help save space, are highly reliable and increase well-being will find improved sales prospects in the coming years. European brand names are leading this movement; from revolving doors and ‘concrete accessories’ to sanitary appliances and designer furniture, European companies have been successful in building a top niche and occupying a dominating market share.

Despite high growth rates, entering the Chinese market remains a challenge for European SMEs. It requires good planning, timing and an effective choice of business partner. To find out more about this diverse market, download The construction sector in China from the EU SME Centre website at www.eusmecentre.org.cn, where you will also be able to find recordings of recent webinars on How to tap into China’s thrust for building? and How to tap into China’s thirst for green building? as well as post enquiries to our in-house experts.

Download the article in pdf.:

EU_SME_Centre_Construction_Sector_September_2013.pdf (91.27 KB)

EU_SME_Centre_Construction_Sector_September_2013.pdf (91.27 KB)